I currently have a long strangle on the QQQ april 6 66/69 currently $15 profit was $530 2 days ago.

No lack of OPTIONS

Moderator: moderators

-

aliassmith

- rank: 5000+ posts

- Posts: 5057

- Joined: Tue Jul 28, 2009 9:50 pm

- Reputation: 2848

- Gender:

Please add www.kreslik.com to your ad blocker white list.

Thank you for your support.

Thank you for your support.

-

PebbleTrader

- rank: 1000+ posts

- Posts: 1633

- Joined: Fri Nov 12, 2010 2:15 am

- Reputation: 15

- Gender:

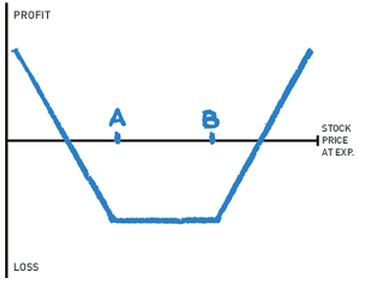

Let's look at aliassmith's Long Strangle:

The Setup

-Buy a put, strike price A

-Buy a call, strike price B

-Generally, the stock price will be between strikes A and B

Break-even At Expiration

There are two break-even points:

-Strike A minus the net debit paid

-Strike B plus the net debit paid.

Maximum Potential Profit:

-Potential profit is theoretically unlimited if the stock goes up.

-If the stock goes down, potential profit may be substantial but limited to

strike A minus the net debit paid.

Maximum Potential Loss

-Potential losses are limited to the net debit paid.

As Time Goes By

-For this strategy, time decay is your mortal enemy. It will cause the value

of both options to decrease, so it's working doubly against you.

Implied Volatility

After the strategy is established, you really want implied volatility to

increase. It will increase the value of both options, and it also suggests an

increased possibility of a price swing. Sweet.

Conversely, a decrease in implied volatility will be doubly painful because it

will work against both options you bought. If you run this strategy, you can

really get hurt by a volatility crunch.

A long strangle gives you the right to sell the stock at strike price A and the

right to buy the stock at strike price B.

The goal is to profit if the stock makes a move in either direction. However,

buying both a call and a put increases the cost of your position, especially

for a volatile stock. So you'll need a significant price swing just to break

even.

The difference between a long strangle and a long straddle is that you

separate the strike prices for the two legs of the trade. That reduces the

net cost of running this strategy, since the options you buy will be out-of-

the-money. The tradeoff is, because you're dealing with an out-of-the-

money call and an out-of-the-money put, the stock will need to move even

more significantly before you make a profit.

The Setup

-Buy a put, strike price A

-Buy a call, strike price B

-Generally, the stock price will be between strikes A and B

Break-even At Expiration

There are two break-even points:

-Strike A minus the net debit paid

-Strike B plus the net debit paid.

Maximum Potential Profit:

-Potential profit is theoretically unlimited if the stock goes up.

-If the stock goes down, potential profit may be substantial but limited to

strike A minus the net debit paid.

Maximum Potential Loss

-Potential losses are limited to the net debit paid.

As Time Goes By

-For this strategy, time decay is your mortal enemy. It will cause the value

of both options to decrease, so it's working doubly against you.

Implied Volatility

After the strategy is established, you really want implied volatility to

increase. It will increase the value of both options, and it also suggests an

increased possibility of a price swing. Sweet.

Conversely, a decrease in implied volatility will be doubly painful because it

will work against both options you bought. If you run this strategy, you can

really get hurt by a volatility crunch.

A long strangle gives you the right to sell the stock at strike price A and the

right to buy the stock at strike price B.

The goal is to profit if the stock makes a move in either direction. However,

buying both a call and a put increases the cost of your position, especially

for a volatile stock. So you'll need a significant price swing just to break

even.

The difference between a long strangle and a long straddle is that you

separate the strike prices for the two legs of the trade. That reduces the

net cost of running this strategy, since the options you buy will be out-of-

the-money. The tradeoff is, because you're dealing with an out-of-the-

money call and an out-of-the-money put, the stock will need to move even

more significantly before you make a profit.

Life is just a journey

-

PebbleTrader

- rank: 1000+ posts

- Posts: 1633

- Joined: Fri Nov 12, 2010 2:15 am

- Reputation: 15

- Gender:

-

PebbleTrader

- rank: 1000+ posts

- Posts: 1633

- Joined: Fri Nov 12, 2010 2:15 am

- Reputation: 15

- Gender:

I think we have mostly covered the basics so we can start talking about strategies. And since there has been no questions that means that everyone is in agreement through silent acquiescence which is wonderful!

But first I want to discuss managing positions by rolling.

But first I want to discuss managing positions by rolling.

Last edited by PebbleTrader on Thu Feb 28, 2013 5:43 pm, edited 1 time in total.

Life is just a journey

-

PebbleTrader

- rank: 1000+ posts

- Posts: 1633

- Joined: Fri Nov 12, 2010 2:15 am

- Reputation: 15

- Gender:

Rolling

Rolling is one of the most common ways to adjust an option position. It's

possible to roll either a long or short option position, but here we'll focus on

the short side.

When you decide to roll, you've changed your outlook on the underlying

stock and fear that your short options are going to be assigned. The

objective is to put off assignment, or even avoid it altogether. It's an

advanced technique, and it's one you need to thoroughly understand

before executing.

When you roll a short position, you're buying to close an existing position

and selling to open a new one. You're tweaking the strike prices on your

options, and / or "rolling" the expiration further out in time. But rolling is

never guaranteed to work. In fact, you might end up compounding your

losses. So exercise caution and don't get greedy.

Rolling is one of the most common ways to adjust an option position. It's

possible to roll either a long or short option position, but here we'll focus on

the short side.

When you decide to roll, you've changed your outlook on the underlying

stock and fear that your short options are going to be assigned. The

objective is to put off assignment, or even avoid it altogether. It's an

advanced technique, and it's one you need to thoroughly understand

before executing.

When you roll a short position, you're buying to close an existing position

and selling to open a new one. You're tweaking the strike prices on your

options, and / or "rolling" the expiration further out in time. But rolling is

never guaranteed to work. In fact, you might end up compounding your

losses. So exercise caution and don't get greedy.

Last edited by PebbleTrader on Fri Mar 01, 2013 3:47 am, edited 1 time in total.

Life is just a journey

Please add www.kreslik.com to your ad blocker white list.

Thank you for your support.

Thank you for your support.

-

PebbleTrader

- rank: 1000+ posts

- Posts: 1633

- Joined: Fri Nov 12, 2010 2:15 am

- Reputation: 15

- Gender:

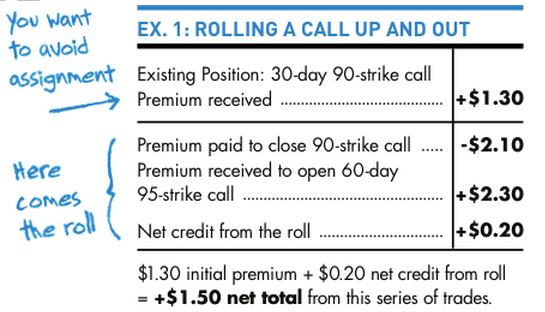

Rolling A Covered Call

Imagine you're running a 30-day covered call on stock XYZ with a strike

price of $90. That means you own 100 shares of XYZ stock, and you've

sold one 90-strike call a month from expiration. When you sold the call, the

stock price was $87.50, and you received a premium of $1.30, or $130

total, since one contract equals 100 shares. Now, with expiration fast

approaching, the stock has gone up to $92. In all probability you will be

assigned and have to sell the stock at $90.

The only way to avoid assignment for sure is to buy back the 90-strike call

before it is assigned, and cancel your obligation. However, the 90-strike

call is now trading for $2.10, so it will hurt a bit to buy it back. To help

offset the cost of buying back the call, you're going to "roll up and out."

That means you want to go "up" in strike price and "out" in time. The idea

is to balance the decrease in premium for selling a higher OTM strike price

versus the greater premium you'll receive for selling an option that is

further from expiration (and thus has more "time value").

Here's an example of how that might work.

Enter a buy-to-close order for the front-month 90-strike call. In the same

trade, you sell to open an OTM 95-strike call (rolling up) that's 60 days

from expiration (rolling out). Due to higher time value, the back-month 95-

strike call will be trading for $2.30. Since you're paying $2.10 to buy back

the front-month call and receiving $2.30 for the back-month call, this trade

can be accomplished for a net credit of $0.20 ($2.30 sale price - $2.10

purchase price) or $20 total.

Let's look at all the good news and bad news surrounding this trade. As

you'll see, it's a double-edged sword.

Since you've raised the strike price to $95, you have more profit potential

on the stock. The obligation to sell was at $90, but now it's at $95. The bad

news is, you had to buy back the front-month call for 80 cents more than

you received when selling it ($2.10 paid to close - $1.30 received to open).

On the other hand, you've more than covered the cost of buying it back by

selling the back-month 95-strike call for more premium. So that's good.

But you have to consider the fact that there are still 60 days before the

new options expire, and you don't really know what will happen with the

stock during that time. You'll just have to keep your fingers crossed.

If the back-month 95-strike short call expires worthless in 60 days, you

wind up with a $1.50 net credit. Here's the math: You lost a total of $0.80

after buying back the 90-strike front-month call. However, you received a

premium of $2.30 for the 95-strike call, so you netted $1.50 ($2.30 back-

month premium - $0.80 front-month loss) or $150 total. That's not a bad

outcome (see Ex.1).

However, if the market makes a big move upward in the next 60 days, you

might be tempted to roll up and out again. But beware.

Every time you roll up and out, you may be taking a loss on the front-

month call. Furthermore, you still have not secured any gains on the back-

month call or on the stock appreciation, because the market still has time

to move against you. And that means you could wind up compounding your

losses. So come to think of it, rolling's not really a double-edged sword. It's

more like a quadruple-edged shaving razor.

Imagine you're running a 30-day covered call on stock XYZ with a strike

price of $90. That means you own 100 shares of XYZ stock, and you've

sold one 90-strike call a month from expiration. When you sold the call, the

stock price was $87.50, and you received a premium of $1.30, or $130

total, since one contract equals 100 shares. Now, with expiration fast

approaching, the stock has gone up to $92. In all probability you will be

assigned and have to sell the stock at $90.

The only way to avoid assignment for sure is to buy back the 90-strike call

before it is assigned, and cancel your obligation. However, the 90-strike

call is now trading for $2.10, so it will hurt a bit to buy it back. To help

offset the cost of buying back the call, you're going to "roll up and out."

That means you want to go "up" in strike price and "out" in time. The idea

is to balance the decrease in premium for selling a higher OTM strike price

versus the greater premium you'll receive for selling an option that is

further from expiration (and thus has more "time value").

Here's an example of how that might work.

Enter a buy-to-close order for the front-month 90-strike call. In the same

trade, you sell to open an OTM 95-strike call (rolling up) that's 60 days

from expiration (rolling out). Due to higher time value, the back-month 95-

strike call will be trading for $2.30. Since you're paying $2.10 to buy back

the front-month call and receiving $2.30 for the back-month call, this trade

can be accomplished for a net credit of $0.20 ($2.30 sale price - $2.10

purchase price) or $20 total.

Let's look at all the good news and bad news surrounding this trade. As

you'll see, it's a double-edged sword.

Since you've raised the strike price to $95, you have more profit potential

on the stock. The obligation to sell was at $90, but now it's at $95. The bad

news is, you had to buy back the front-month call for 80 cents more than

you received when selling it ($2.10 paid to close - $1.30 received to open).

On the other hand, you've more than covered the cost of buying it back by

selling the back-month 95-strike call for more premium. So that's good.

But you have to consider the fact that there are still 60 days before the

new options expire, and you don't really know what will happen with the

stock during that time. You'll just have to keep your fingers crossed.

If the back-month 95-strike short call expires worthless in 60 days, you

wind up with a $1.50 net credit. Here's the math: You lost a total of $0.80

after buying back the 90-strike front-month call. However, you received a

premium of $2.30 for the 95-strike call, so you netted $1.50 ($2.30 back-

month premium - $0.80 front-month loss) or $150 total. That's not a bad

outcome (see Ex.1).

However, if the market makes a big move upward in the next 60 days, you

might be tempted to roll up and out again. But beware.

Every time you roll up and out, you may be taking a loss on the front-

month call. Furthermore, you still have not secured any gains on the back-

month call or on the stock appreciation, because the market still has time

to move against you. And that means you could wind up compounding your

losses. So come to think of it, rolling's not really a double-edged sword. It's

more like a quadruple-edged shaving razor.

Life is just a journey

-

PebbleTrader

- rank: 1000+ posts

- Posts: 1633

- Joined: Fri Nov 12, 2010 2:15 am

- Reputation: 15

- Gender:

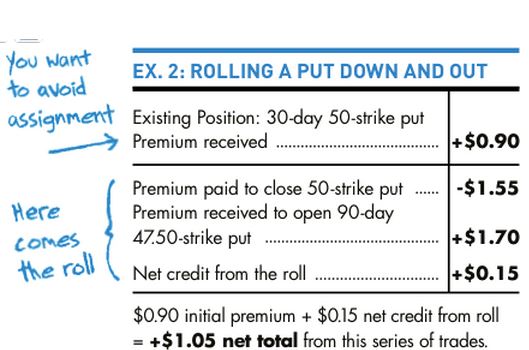

Rolling A Cash-Secured Put

To avoid assignment on a short put, the roll here is "down and out."

For example, let's say you've sold a 30-day cash-secured put on stock XYZ

with a strike price of $50. And let's say you received $0.90 for the put

when the stock was trading at $51. Now, close to expiration, the stock has

dropped and it's trading at $48.50.

The only way to avoid assignment for sure is to buy back the front-month

50-strike put before it is assigned, and cancel your obligation. The problem

is, the front-month put you originally sold for $0.90 is now trading at $1.55.

Here's how you roll.

Enter a buy-to-close order for the front-month 50-strike put. In the same

trade, you sell to open a back-month 47.50-strike put (rolling down), 90

days from expiration (rolling out) which is trading for $1.70. By doing this,

you'll receive a net credit of $0.15 ($1.70 back-month sale price - $1.55

front-month purchase price) or $15 total.

You were able to roll for a net credit even though the back-month put is

further OTM because of the considerable increase in time value of the 90-

day option.

If the 47.50-strike put expires worthless, when all is said and done in 90

days, you'll net $1.05. Here's the math: You lost a total of $0.65 on the

front-month put ($1.55 paid to close - $0.90 received to open). However,

you received a premium of $1.70 for the 47.50-strike put, so you netted

$1.05 ($1.70 back month premium - $0.65 front-month loss) or $105 total

(see Ex.2 above).

However, every time you roll down and out, you may be taking a loss on

the front-month put. Furthermore, you have not secured any gains on the

back-month put because the market still has time to move against you.

And that means you could wind up compounding your losses.

To avoid assignment on a short put, the roll here is "down and out."

For example, let's say you've sold a 30-day cash-secured put on stock XYZ

with a strike price of $50. And let's say you received $0.90 for the put

when the stock was trading at $51. Now, close to expiration, the stock has

dropped and it's trading at $48.50.

The only way to avoid assignment for sure is to buy back the front-month

50-strike put before it is assigned, and cancel your obligation. The problem

is, the front-month put you originally sold for $0.90 is now trading at $1.55.

Here's how you roll.

Enter a buy-to-close order for the front-month 50-strike put. In the same

trade, you sell to open a back-month 47.50-strike put (rolling down), 90

days from expiration (rolling out) which is trading for $1.70. By doing this,

you'll receive a net credit of $0.15 ($1.70 back-month sale price - $1.55

front-month purchase price) or $15 total.

You were able to roll for a net credit even though the back-month put is

further OTM because of the considerable increase in time value of the 90-

day option.

If the 47.50-strike put expires worthless, when all is said and done in 90

days, you'll net $1.05. Here's the math: You lost a total of $0.65 on the

front-month put ($1.55 paid to close - $0.90 received to open). However,

you received a premium of $1.70 for the 47.50-strike put, so you netted

$1.05 ($1.70 back month premium - $0.65 front-month loss) or $105 total

(see Ex.2 above).

However, every time you roll down and out, you may be taking a loss on

the front-month put. Furthermore, you have not secured any gains on the

back-month put because the market still has time to move against you.

And that means you could wind up compounding your losses.

Life is just a journey

-

PebbleTrader

- rank: 1000+ posts

- Posts: 1633

- Joined: Fri Nov 12, 2010 2:15 am

- Reputation: 15

- Gender:

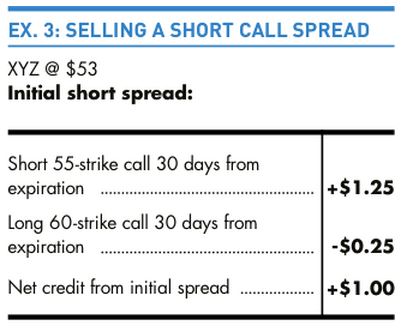

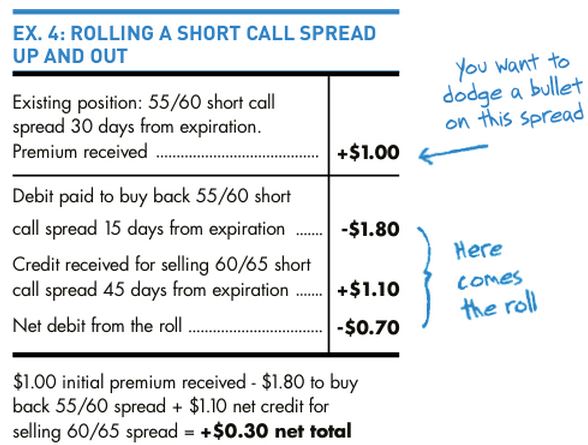

Rolling A Short Call Spread

Rolling a spread works much the same way as rolling an individual option. You will most likely be moving out in time and moving the strike prices either up or down. The difference is you will be trading four different options in one trade instead of two. In other words, you're closing two existing options and opening two new ones.

Now imagine you're bearish on stock XYZ, and it's trading at $53. You might decide to sell a 55/60 short call spread 30 days from expiration, and receive a credit of $1. (You can see how we arrived at the $1 credit in Ex.3, and from this point forward, we'll just focus on the net credit or debit to trade a spread.)

But what if your forecast was wrong, the stock makes a bullish short-term move to $55.50 with 15 days remaining until expiration, and the net cost to buy the spread back is now $1.80? If you're still convinced your forecast is correct and the stock price won't continue to rise, you can roll the spread's strikes up in price and roll expiration out in time.

To do so, you would pay the $1.80 to buy back the 55/60 short call spread and simultaneously sell another short call spread with a short strike of 60, a long strike of 65 and 45 days until expiration. For the 45-day 60/65 strike short call spread you receive a credit of $1.10.

Now instead of being down $0.80 on the trade, if the stock is below $60 at the new expiration date, you'll be up a total of $0.30 ($1.00 net credit to open the 55/60 spread - $1.80 net debit to close the 55/60 spread + $1.10 net credit to open the 60/65 spread = $0.30).

At this point, you really have to hope your forecast is correct and the stock stays below $60. You'll only be up $0.30 on the trade and that's if everything works out as planned. So if the stock continues to make a bullish move beyond the 60 short strike, things could go south in a hurry.

We can't emphasize this enough: when you roll any option, you may be setting yourself up to compound your losses. There's no shame in ditching your position instead of rolling if you're not extremely confident your forecast is correct.

Rolling a spread works much the same way as rolling an individual option. You will most likely be moving out in time and moving the strike prices either up or down. The difference is you will be trading four different options in one trade instead of two. In other words, you're closing two existing options and opening two new ones.

Now imagine you're bearish on stock XYZ, and it's trading at $53. You might decide to sell a 55/60 short call spread 30 days from expiration, and receive a credit of $1. (You can see how we arrived at the $1 credit in Ex.3, and from this point forward, we'll just focus on the net credit or debit to trade a spread.)

But what if your forecast was wrong, the stock makes a bullish short-term move to $55.50 with 15 days remaining until expiration, and the net cost to buy the spread back is now $1.80? If you're still convinced your forecast is correct and the stock price won't continue to rise, you can roll the spread's strikes up in price and roll expiration out in time.

To do so, you would pay the $1.80 to buy back the 55/60 short call spread and simultaneously sell another short call spread with a short strike of 60, a long strike of 65 and 45 days until expiration. For the 45-day 60/65 strike short call spread you receive a credit of $1.10.

Now instead of being down $0.80 on the trade, if the stock is below $60 at the new expiration date, you'll be up a total of $0.30 ($1.00 net credit to open the 55/60 spread - $1.80 net debit to close the 55/60 spread + $1.10 net credit to open the 60/65 spread = $0.30).

At this point, you really have to hope your forecast is correct and the stock stays below $60. You'll only be up $0.30 on the trade and that's if everything works out as planned. So if the stock continues to make a bullish move beyond the 60 short strike, things could go south in a hurry.

We can't emphasize this enough: when you roll any option, you may be setting yourself up to compound your losses. There's no shame in ditching your position instead of rolling if you're not extremely confident your forecast is correct.

Life is just a journey

-

aliassmith

- rank: 5000+ posts

- Posts: 5057

- Joined: Tue Jul 28, 2009 9:50 pm

- Reputation: 2848

- Gender:

PebbleTrader wrote:Let's look at aliassmith's Long Strangle:

The Setup

-Buy a put, strike price A

-Buy a call, strike price B

-Generally, the stock price will be between strikes A and B

Break-even At Expiration

There are two break-even points:

-Strike A minus the net debit paid

-Strike B plus the net debit paid.

Maximum Potential Profit:

-Potential profit is theoretically unlimited if the stock goes up.

-If the stock goes down, potential profit may be substantial but limited to

strike A minus the net debit paid.

Maximum Potential Loss

-Potential losses are limited to the net debit paid.

As Time Goes By

-For this strategy, time decay is your mortal enemy. It will cause the value

of both options to decrease, so it's working doubly against you.

Implied Volatility

After the strategy is established, you really want implied volatility to

increase. It will increase the value of both options, and it also suggests an

increased possibility of a price swing. Sweet.

Conversely, a decrease in implied volatility will be doubly painful because it

will work against both options you bought. If you run this strategy, you can

really get hurt by a volatility crunch.

A long strangle gives you the right to sell the stock at strike price A and the

right to buy the stock at strike price B.

The goal is to profit if the stock makes a move in either direction. However,

buying both a call and a put increases the cost of your position, especially

for a volatile stock. So you'll need a significant price swing just to break

even.

The difference between a long strangle and a long straddle is that you

separate the strike prices for the two legs of the trade. That reduces the

net cost of running this strategy, since the options you buy will be out-of-

the-money. The tradeoff is, because you're dealing with an out-of-the-

money call and an out-of-the-money put, the stock will need to move even

more significantly before you make a profit.

Well that chart is the typical chart for the results at expiration. IN the mean time the options will have a current value that can put you in profits even when you are still in the middle.

Trade Your Way as Long as It Makes Money!

-

PebbleTrader

- rank: 1000+ posts

- Posts: 1633

- Joined: Fri Nov 12, 2010 2:15 am

- Reputation: 15

- Gender:

The above concepts apply to any type of two-legged trade, not just short

spreads. You can also roll straddles, combinations, front spreads and back

spreads. You can even roll one-half of four-legged trades that consist of two

spreads, like iron condors and double diagonals.

Rolling spreads is something iron condor and double diagonal traders

absolutely must understand, since both strategies consist of two short spreads

(one with calls and one with puts).

When you roll a spread, make sure you pull it off all in one trade to help

protect against stock movement between the time you close one spread and

open another.

spreads. You can also roll straddles, combinations, front spreads and back

spreads. You can even roll one-half of four-legged trades that consist of two

spreads, like iron condors and double diagonals.

Rolling spreads is something iron condor and double diagonal traders

absolutely must understand, since both strategies consist of two short spreads

(one with calls and one with puts).

When you roll a spread, make sure you pull it off all in one trade to help

protect against stock movement between the time you close one spread and

open another.

Life is just a journey

Please add www.kreslik.com to your ad blocker white list.

Thank you for your support.

Thank you for your support.