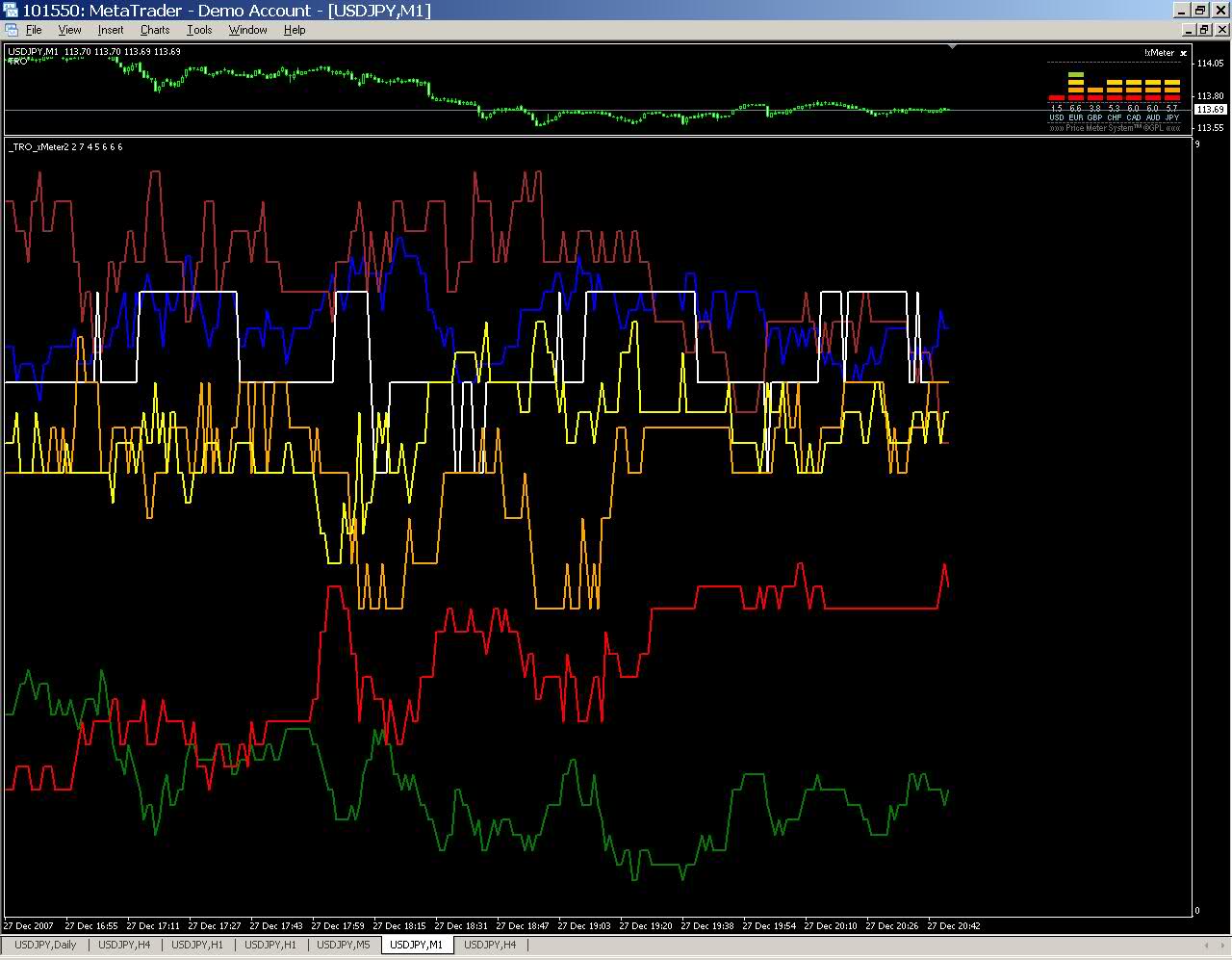

Postby TheRumpledOne » Thu Dec 27, 2007 7:52 pm

I turned the xMeter into a chart so you can see the history of the strength/weakness of the currencies.

Since this uses bid/ask info, when you load it up, it will NOT plot any history but will start from the load time. Just leave it running and the chart will fill out.

-

Attachments

-

TRO_xMeter.zip

TRO_xMeter.zip- (7.34 KiB) Downloaded 327 times

Last edited by

TheRumpledOne on Mon Apr 07, 2008 1:06 pm, edited 1 time in total.

IT'S NOT WHAT YOU TRADE, IT'S HOW YOU TRADE IT!

Please do NOT PM me with trading or coding questions, post them in a thread.